G7 Sanctions: A Force Behind Shifting Energy Sector Dynamics

The Group of Seven (G7)—comprising Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States—remains the primary architect of global economic sanctions.

Sanctions occupy the strategic middle ground between diplomacy and active warfare. They exert pressure—complementing diplomacy and pushing back on armed conflict. Their success depends on corporations and investors keeping abreast of a constantly changing situation.

For investors and global businesses, navigating the landscape requires distinguishing between comprehensive embargoes (total blocks) and targeted sanctions (specific restrictions) on targeted critical sectors as well as specific financial institutions. Below, we lay out the G7 sanctions landscape today—current regulatory environment, industries most affected, and emerging market opportunities resulting from these geopolitical shifts.

Countries Affected by G7 Sanctions

U.S. sanctions programs are divided into two types: broad-based, geographically-oriented, referred to as Comprehensively Embargoed countries or Comprehensively Sanctioned Countries; and targeted sanctions.

Comprehensively Sanctioned Countries by USA

- Cuba

- Iran

- North Korea

- Russia

- Crimea, Donetsk, and Luhansk regions of Ukraine

G7 Sanctioned Countries

The following nations face targeted sanctions from one or more G7 members.

| Region | Countries Affected |

|---|---|

| Americas | Nicaragua, Venezuela, Guatemala, Haiti |

| Europe/Eurasia | The Balkans, Belarus, Moldova, Türkiye |

| Middle East/Asia | Afghanistan, Burma (Myanmar), Hong Kong, Iraq, Lebanon, Syria, Yemen, Chinese Military Companies |

| Africa | Central African Republic, Democratic Republic of the Congo, Ethiopia, Libya, Mali, Somalia, South Sudan, Sudan, Zimbabwe, Burundi, Guinea, Niger, Tunisia |

Industries Impacted by Sanctions

Common measures within sanctions include Asset Freezes—blocking the funds of an entire country or specific persons, Travel Bans—preventing individuals from entering, Arms Embargoes—prohibiting the sale of weapons to the country, Energy Embargoes —prohibiting the import of oil, petrochemicals, gas from sanctioned countries or energy processing/ technologies/services and Embargoes of other sectors. The widest ranging economic disruptions of sanctions occur in the Financial and Energy sectors.

Energy Sector

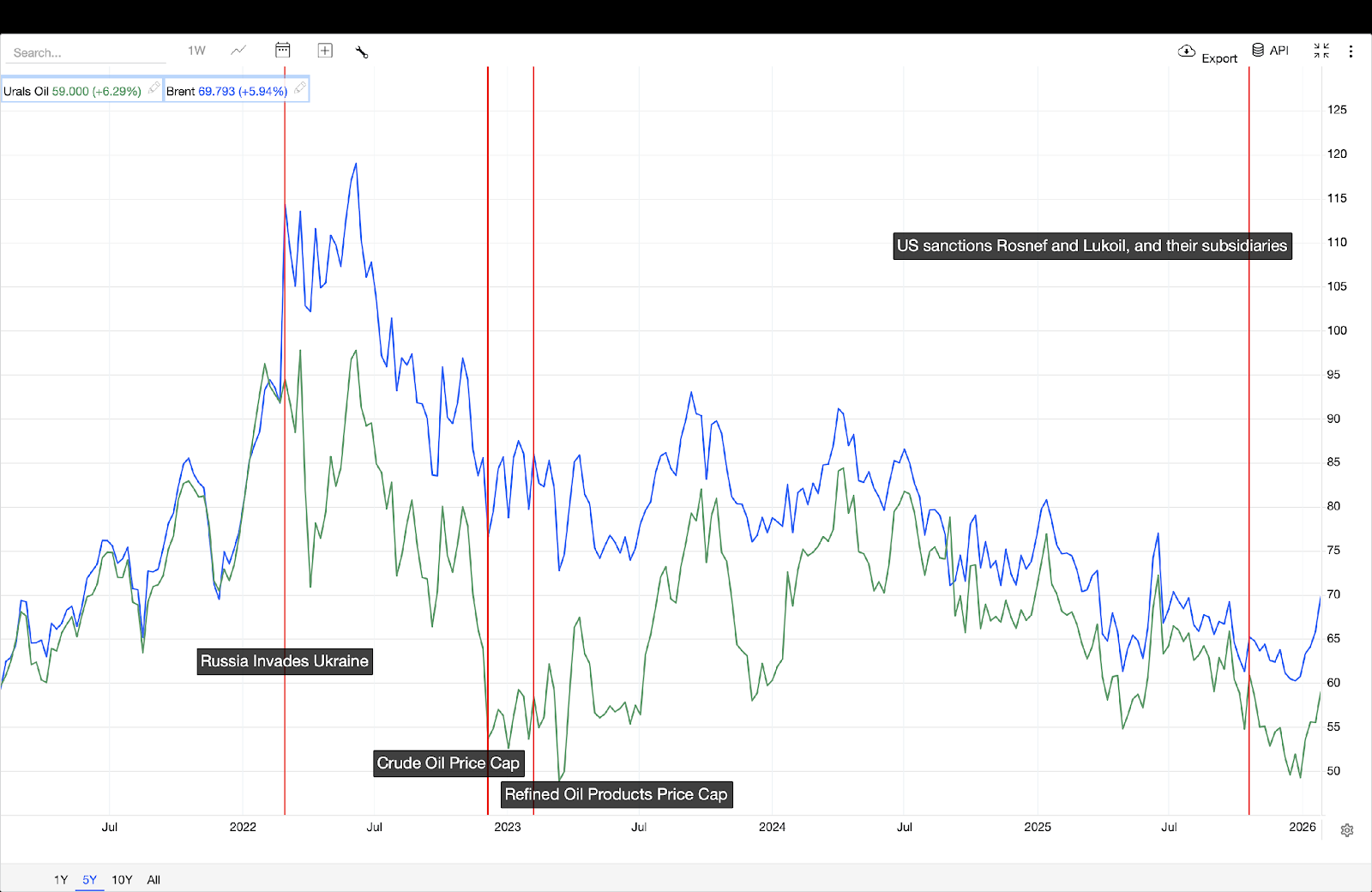

Oil, gas, and oil products are undoubtedly among the most impacted sectors due to sanctions. Russia, Venezuela, and Iran have in recent history been forced to sell oil below market prices, as buyers of these countries’ oil began demanding lower prices to compensate for the elevated risk and higher logistical costs posed by sanctions.

The latest sanctions package from the EU introduced a full ban on Russian liquid natural gas imports from 1 January 2027. This gradual phase-out began on 17 June 2025.

Altogether, sanctions have created a series of distortions in the oil markets. First, market transparency has deteriorated as crude from Iran, Russia, and Venezuela is increasingly traded in the shadow, providing less information regarding current and future oil production, exports, and pricing. Simultaneously and strategically, major importers like China have reduced the public release of data regarding their oil purchases. Second, sanctions and price caps have introduced significant inefficiencies. To evade restrictions, shipments are diverted to alternative, longer routes, driving up logistical costs. This increase in transit time per barrel requires a larger fleet of vessels just to maintain the same volume of crude transport.

Third - and equally critical - to evade the price cap, oil is being traded in low-quality infrastructure. Sanctioned crude is frequently transported on older, poorly regulated vessels, which significantly increases the risk of oil spills and environmental disasters. This is an important cost of sanctions for European nations, compounding the financial burden of importing crude from significantly more distant suppliers.

Urals and Brent oil prices over time

Price of oil (USD/bbl)

Financial Sector

The financial sector has been deeply impacted by secondary sanctions. This type of sanctions targets third parties, including individuals, financial institutions, or other firms that do business with a designated target of sanctions, regardless of where those third parties are located. The U.S. is the primary architect of this type of sanctions, which effectively presents a binary choice in which either third parties stop engaging in transactions with the sanctioned entity, or keep business dealings with them and risk losing access to the U.S. economy and financial system.

The United States and its allies regulate the world’s most widely used reserve and payment currencies and financial networks such as the Society for Worldwide Interbank Financial Telecommunication (SWIFT), leaving little room for rerouting monetary flows, which is why large-scale circumvention of financial sanctions via third markets, even those of China, is extremely difficult.

While China’s renminbi (RMB) has gained influence as an alternative payment currency, its financial system remains underdeveloped compared to the existing networks, making sanctions circumvention highly costly. The same logic applies to the BRICS block, whose alternatives are still in their infancy and lack the scale to fundamentally undermine advanced economies’ financial sanctions.

For the same reasons stated above, the possibility of being excluded from the US financial system for maintaining or performing financial transactions with sanctioned entities or individuals is threatening enough to largely prevent these activities. Financial institutions sometimes over-comply, terminating services for legitimate businesses in high-risk regions merely to avoid potential scrutiny.

Beneficiaries of Sanction Regimes

In the case of sanctions and price caps imposed on the Russian Oil Industry, the American Enterprise Institute lists a group of strategies that the country developed to avoid them, from which it is possible to understand where opportunities arise.

Price caps are applied by operators within the Price Cap Coalition - including G7, EU and Australia - that provide transport and insurance services for the transport of Russian oil. Russia’s primary strategy has been to acquire its own vessels to transport crude oil and oil products, known as a “shadow fleet”. As of September 2025, the Center for Research on Energy and Clean Air estimates shadow tankers delivered 69% of Russian crude oil exports.

New shipping companies have also been formed. This occurs in countries like Turkey, China and Greece, which buy vessels - many of them old - to transport Russian oil. These firms, surging as new transport service providers, are among the winners of sanctions, as well as non-Western shipping insurance providers.

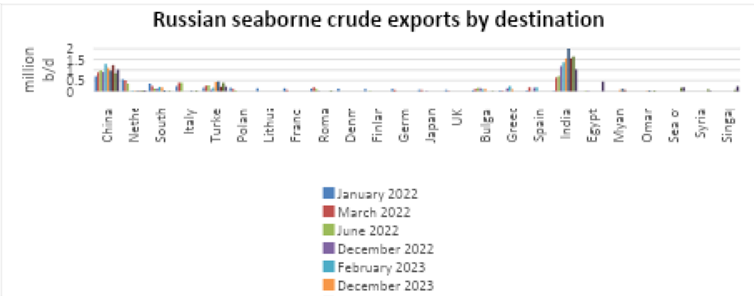

On the other side, Russia’s Urals crude, whose main market was European customers, had to look for new markets to replace the previous European customers, facing large discounts to attract Indian clients. For Russian Pacific crude, primary markets are China and other Asian customers. As it can be observed in the chart below, China and India are the two countries that have benefited the most from discounts in Russian crude prices, especially India who started acquiring Russian crude after sanctions were imposed, and assumed the role as refiner of oil products to re-export to other states, including European countries—to tackle this mechanism, the EU 18th sanctions package included an import ban on refined oil products derived from Russian crude.

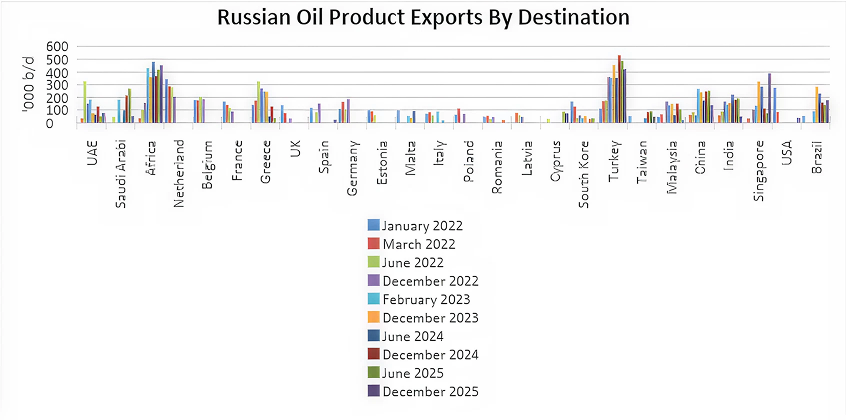

In the case of Russian oil products, Turkey has stood out by notably increasing its imports to become the main destination of Russian oil products exports. Singapore, China, India, Brazil, and African countries (mainly Egypt, Tunisia, and Libya), also became important markets for these products, and until the Strait of Hormuz closed, UAE and Saudi Arabia as well.

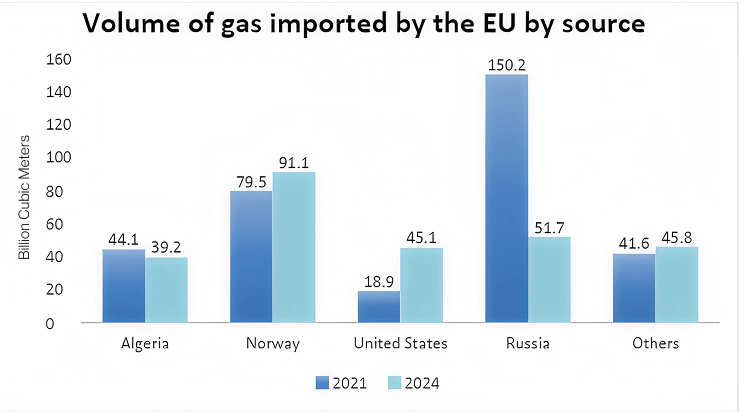

American and Norwegian-owned oil and gas producers have also benefited from sanctions regarding the energy sector in Russia. The European Union has been changing its imports of pipeline gas from Russia, in favour of gas provided mainly by Norway and the US. The chart below shows the volume of gas imported by the EU in 2021, the year before sanctions of the Russian energy sector started, and 2024, This demonstrates that the United States became the largest supplier of LNG to Europe, accounting for almost 45% of their total imports of LNG, and what is more, imports from the US in 2024 were more than double what they were in 2021.

Canadian crude oil producers benefit from U.S. sanctions on Venezuelan energy. Before sanctions, the U.S. was the largest consumer of Venezuelan heavy crude for Gulf Coast refineries, which were created with the complexity and equipment necessary to process heavy crude. However, after sanctions, Gulf Coast refineries have replaced most of Venezuelan crude with Canadian heavy oil, according to a S&P Global report.

Scenario Analysis: Who Benefits is in the case of easing sanctions against Venezuela

While much of the market focuses on the imposition of sanctions, the potential removal of sanctions offers significant opportunities, particularly in Venezuela.

Current U.S. sanctions target energy and metal sectors, focusing on the state gold company (Minerven) and state energy company (PdVSA). However, the political landscape shifted following the capture of Nicolas Maduro. With President Trump announcing plans to trade Venezuelan crude, the market is preparing for a reopening, attracting oil and gas companies to the country, such as Halliburton Company, Eni, Repsol, among others. Nonetheless, companies require political and fiscal stability to be willing to invest the large amounts needed to recover the industry.

If these companies start investing, a chain effect will occur in the slow recovery of related sectors such as infrastructure, electricity, equipment, construction, engineering, and services for the grid recovery and modernization, such as Quanta Services, Inc. (NYSE: PWR)

Should the country stabilize, other types of companies may be willing to resume operations in Venezuela, including airlines such as Copa Holdings (NYSE: CPA), consumer goods companies like The Procter & Gamble Company (NYSE: PG), Unilever (LSE: ULVR), and international banks.

BITA's Proprietary Data Team analyzes revenue streams across all areas of all industries. Our 90 Thematic Universes (with 396 investment themes or sectors) range from finance, technology, sustainability, social impact, food, health, leisure, sports, and culture to full coverage of controversial business involvement.

BITA covers the main industries and companies that could reestablish operations in Venezuela as sanctions ease, providing insights and indices for investors ready to increase exposure in companies that would benefit the most.

References

1 - UK Sanctions. December 2025. https://www.gov.uk/government/collections/uk-sanctions#current-uk-sanctions-regimes

2 - EU Sanctions Map. December 21, 2025. https://www.sanctionsmap.eu/#/main?checked=

3 - U.S. DEPARTMENT OF THE TREASURY-Sanctions Programs and Country Information. https://ofac.treasury.gov/sanctions-programs-and-country-information

4 - U.S. DEPARTMENT OF THE TREASURY. Treasury Sanctions Major Russian Oil Companies, Calls on Moscow to Immediately Agree to Ceasefire. October 22, 2025. https://home.treasury.gov/news/press-releases/sb0290

5 - US Prohibited exports, imports, and sales to or from certain countries of defense articles and defense services. January 14, 2026. https://www.ecfr.gov/current/title-22/chapter-I/subchapter-M/part-126/section-126.1

6 - Princeton University-OFFICE OF THE DEAN FOR RESEARCH. OFAC Sanctioned Countries. January 2026. https://orpa.princeton.edu/export-controls/sanctioned-countries

7 - Centre for Research on Energy and Clean Air (CREA), 2023. https://energyandcleanair.org/russia-sanction-tracker/

8 - UK Parliament. Sanctions against Russia: What has changed in 2025? November 28, 2025. https://commonslibrary.parliament.uk/research-briefings/cbp-10342/

9 - Sanctions Advisory. Understanding the Nuances: A Comparison of EU, UK, and US Sanctions Regimes. OCTOBER 30, 2025. https://sanctionsadvisory.dk/understanding-the-nuances-a-comparison-of-eu-uk-and-us-sanctions-regimes/

10 - American Enterprise Institute. Sanctions on Russia and the Splintering of the World Oil Market. February 2024. https://www.aei.org/wp-content/uploads/2024/02/Sanctions-on-Russia-and-the-Splintering-of-the-World-Oil-Market.pdf?x97961

11 - S&P Global. INTERACTIVE: Global oil flow tracker (Russian exports). Dec. 3, 2025. https://www.spglobal.com/energy/en/news-research/latest-news/crude-oil/072122-interactive-global-flow-tracker-recording-changes-russian-oil-exports

12 - Council of the EU and the European Council. Where does the EU’s gas come from? November 13, 2025. https://www.consilium.europa.eu/en/infographics/where-does-the-eu-s-gas-come-from/

13 - Centre for Research on Energy and Clean Air (CREA). October 14, 2025. September 2025 — Monthly analysis of Russian fossil fuel exports and sanctions. https://energyandcleanair.org/september-2025-monthly-analysis-of-russian-fossil-fuel-exports-and-sanctions/

14 - CBS News. November 20, 2025. Sanctions have choked Russia's oil industry, a key source of Kremlin funds, U.S. Treasury finds. https://www.cbsnews.com/news/sanctions-choked-russia-oil-industry-a-key-source-of-kremlin-funds/

15 - Oilprice.com. Europe’s New Oil Sanctions Are Squeezing Russian Revenues. Jan 19, 2026. Europe’s New Oil Sanctions Are Squeezing Russian Revenues | OilPrice.com

16 - European Commission. Sanctions on energy. October 23, 2025 https://commission.europa.eu/topics/eu-solidarity-ukraine/eu-sanctions-against-russia-following-invasion-ukraine/sanctions-energy_en

17 - Center for Strategic & International Studies. Back & Forth 3: Do Sanctions Work? March 19, 2025. https://www.csis.org/analysis/back-forth-3-do-sanctions-work

18 - IEA. Gas Market Report, Q1-2026. January 2026. https://iea.blob.core.windows.net/assets/98d3c7fc-d2ee-479a-aa8f-c02da1c8a4b8/GasMarketReport%2CQ1-2026.pdf

19 - Medium. When Sanctions Meet Strategy: How India-Russia Oil Trade Moves Through Dubai & the Gulf. October 15, 2025. https://medium.com/@2020.prerak/when-sanctions-meet-strategy-how-india-russia-oil-trade-moves-through-dubai-the-gulf-e0af0fb9cc72

20 - Trading Economics. Urals Oil. January 30, 2025. https://tradingeconomics.com/commodity/urals-oil

21 - US Congress.Venezuela: Overview of U.S. Sanctions Policy. January 16, 2026. https://www.congress.gov/crs-product/IF10715#:~:text=The%20U.S.%20Department%20of%20the,to%20face%20narco%2Dterrorism%20charges.

22 - S&P Global. Venezuela: The Oil Trade, And Who Stands To Benefit. January 13, 2026. https://www.spglobal.com/ratings/en/regulatory/article/venezuela-the-oil-trade-and-who-stands-to-benefit-s101664836