Luxury Sector: Structural Strength Amid Macroeconomic Volatility

A Sector Under Pressure — With Long-Term Strength

Historically, the luxury sector has demonstrated remarkable resilience across a wide spectrum of macroeconomic headwinds. This enduring stability is built on several foundational virtues: deep brand equity, artificial scarcity, and exceptional pricing power that allows premier houses to pass rising input costs onto consumers whose purchasing behaviour is largely insulated from everyday macroeconomic pressures.

The Iran war, which erupted in late February 2026, dealt the sector a severe near-term blow. Approximately $100 billion in market value was erased from Europe's top 10 luxury house stocks in March alone ($176 billion by June), with Hermès falling roughly 18%, Ferrari declining over 30% from its 2025 highs, and LVMH’s first-quarter organic growth halved following the conflict’s impact on the Middle East.

In June, with the memorandum of understanding (MoU) between the United States and Iran, luxury stocks rose slightly between 3% and 5% following the announcement. This initial wave of market optimism was primarily driven by the reopening of the Strait of Hormuz. However, this relief appears to be short-lived due to growing concerns about non-compliance with the terms of the MoU.

Although the geopolitical landscape remains uncertain, for investors and market observers willing to look beyond the near-term noise, it is essential to evaluate the luxury sector today, specifically companies focused on upper and ultra-luxury products and services, whose fundamentals comprise a solid engine for long-term growth.

Beyond the War: The Structural Headwinds Luxury Confronts

In recent years, the luxury sector witnessed a significant strategic pivot as major brands aggressively targeted aspirational consumers. Driven by the relentless pressure of public markets to deliver continuous earnings growth, companies capitalized on a unique financial anomaly during the COVID-19 pandemic. Flush with temporary liquidity from stimulus checks, halted student loans, and a lack of travel expenses, the middle class temporarily emerged as a highly lucrative demographic.

To capture this unprecedented wave of demand, many prestigious houses shifted their focus toward volume. They leaned heavily into entry-level products, trend-driven streetwear, and logomania, aiming to attract younger, aspirational buyers. While this approach generated a massive short-term revenue boom, it fundamentally altered their business models and brand perception.

As these temporary macroeconomic tailwinds faded around 2023, the strategy severely backfired. Brands that overexposed themselves to the mass market suffered a profound loss of pricing power as the aspirational consumer retreated. Bain & Company estimates that the addressable consumer base pool has contracted from roughly 400 million in 2022 to 340 million in 2025, with a further loss of 20–30 million consumers. Worse still, the ubiquitous nature of their entry-level products alienated their core, high-net-worth clientele. Ultimately, by chasing short-term volume, these companies diluted their exclusivity and sacrificed the very soul of luxury.

In contrast, top-tier customers have maintained their spending habits. Brands operating at the zenith of the market—such as Hermès, Ferrari, and Brunello Cucinelli—continue to demonstrate extraordinary pricing power. Because their business models are anchored in genuine scarcity, uncompromising craftsmanship, and a highly exclusive clientele, they were not affected by the pullback of the mass-luxury market. This structural divergence has altered institutional investment strategies. Carmignac, one of Europe’s premier independent asset managers, perfectly illustrated this shift by confirming its portfolio holds positions in Hermès and Ferrari, while deliberately bypassing broader conglomerates like LVMH.

The Wealth Engine Continues to Grow

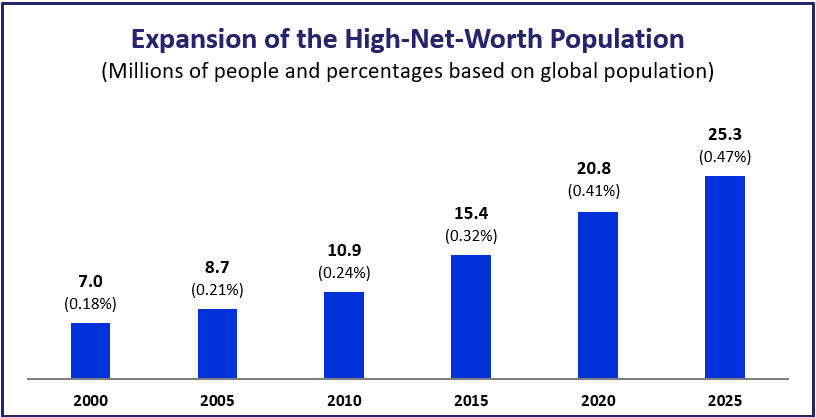

Despite the contraction in the aspirational customer base, the demographic engine at the very top of the wealth pyramid continues to expand. In 2000, the world counted approximately 7 million HNWIs. By 2025, that figure had risen to 25.3 million, tripling in size and representing 0.47% of the adult population, up from 0.18% in 2000.

This demographic growth is not merely a numerical milestone but a structural foundation for the luxury market. Unlike millionaires whose wealth may be concentrated in illiquid real estate, the liquid millionaire class has the purchasing power to acquire ultra-luxury assets at any time. This pool of capital acts as a permanent buffer for the luxury industry, ensuring that even during some economic downturns, demand for the world’s most exclusive goods remains supported.

In 2025, Ultra High Net Worth Individuals (UHNWIs) accounted for nearly 47% of all personal luxury sales, up from 35% in 2021. This concentration has led the industry to move away from mass-market luxury in favor of what Bain & Company describes as “Absolute Luxury” — where the client is no longer just a consumer but a strategic partner in the brand’s legacy, with an emphasis on intimacy, personalization, and renewed attention to well-being.

Luxury as a Hard Asset — Tested by Fire

In the volatile financial environment of the 2020s, upper and ultra-luxury goods emerged as legitimate alternative asset classes. A Patek Philippe Nautilus is increasingly viewed not as a purchase but as a “hard asset” comparable to gold or fine art. Historical data show that these items have outperformed many traditional stock indices over the last decade, particularly during inflationary periods.

The principle of controlled scarcity underpins this investment thesis. Unlike mass-market goods, ultra-luxury houses deliberately restrict supply regardless of demand, creating secondary markets where items often trade at significant premiums over retail prices. In 2025, the Hermès Birkin 25 retailed between $11,000 and $12,000, while pristine examples frequently commanded $24,000 to $30,000 on the resale market— a premium driven by waitlists extending beyond two years. In late 2024, Ferrari reaffirmed its status at the pinnacle of automotive excellence with the announcement of the F80 hypercar, restricted to just 799 units. Although the initial base price was approximately $3.7 million, secondary market valuations had risen to $5.5 million by early 2026.

Critically, the upper and ultra-luxury sectors have demonstrated a remarkable ability to pass on costs to consumers. As inflation rose between 2021 and 2025, Hermès successfully implemented price increases of 20% or more without losing its core customer base. This pricing power was demonstrated by U.S. trade politics in 2025, when import tariffs threatened European goods; luxury houses swiftly offset these expenses through targeted price adjustments, experiencing only modest demand effects among their top-tier clientele.

Where the Pain Is — and Where It Isn’t

The Middle East: A Fragile Reopening Amidst Uncertainty

Before the recent geopolitical friction, the Middle East — specifically Dubai and Riyadh — had solidified its status as one of the sector’s fastest-growing regions. A young, ultra-wealthy population viewed luxury consumption as a central pillar of their lifestyle, and massive infrastructure investments were drawing global brands.

The outbreak of the Iran conflict certainly disrupted this trajectory earlier in the year. During the height of the tensions, Ferrari temporarily suspended deliveries to the region, Kering reported an 11% decline in Middle Eastern retail revenue in Q1, and Hermès cited the region as “significantly affected”. With the Strait of Hormuz facing blockades and commercial flights disrupted at the time, the tourist-dependent luxury ecosystem in the Gulf absorbed a severe short-term shock.

Following the June 17 Memorandum of Understanding (MoU) between the US and Iran, the reopening of the Strait of Hormuz, and the lifting of the US naval blockade, regional logistics have begun to normalize.

However, due to the critical state of the MoU, geopolitical risk premiums are notoriously difficult to shake off. Until secure transit routes are permanently guaranteed and regional stability is demonstrably sustained, major luxury houses are expected to pause their capital expenditures. For now, the luxury market remains deeply uncertain in the region.

China: Maturing, Not Declining

Following years of post-pandemic prosperity and real estate uncertainty, the Chinese consumer has become more rational and selective. The era of conspicuous logomania is fading, replaced by a preference for craftsmanship, luxury travel, wellness, and fine dining.

BNP Paribas projects the Chinese market to grow approximately 6% in 2026, with a more robust 10% compound annual growth rate from 2027 to 2031. J.P. Morgan’s fieldwork confirms that Chinese HNWIs are shifting toward “quiet luxury” — understated style over ostentatious branding — while aspirational consumers are prioritizing experiences and smaller-ticket items. Chinese consumers are also increasingly favoring domestic luxury brands, such as the high-end heritage collections of Chow Tai Fook, driven by national pride and competitive quality.

The United States: Resilient Growth Engine

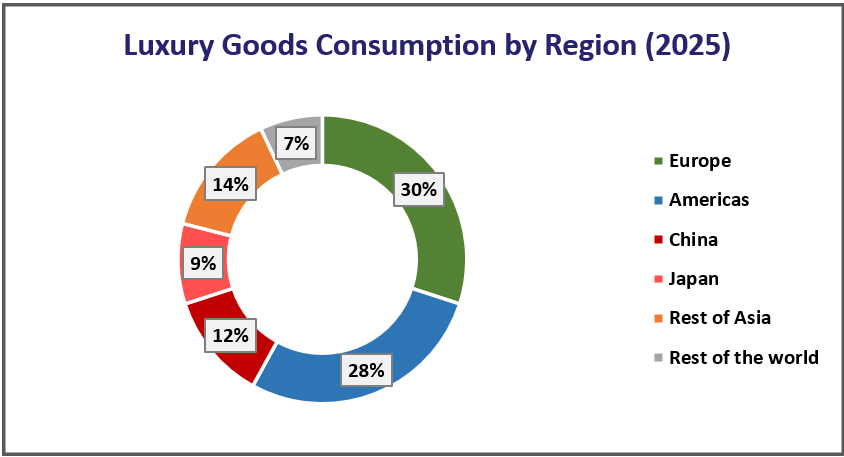

The US has reclaimed its role as the world’s primary growth engine for luxury. This positioning is fundamentally underpinned by domestic wealth creation, fueled by a tech-heavy stock market and the broader AI boom. American millionaires have driven a surge in domestic luxury spending. Major luxury conglomerates report that the Americas account for approximately 28% of global luxury goods consumption.

According to Bain & Company, “luxury spending is on the rise across apparel, hard luxury, and to a lesser extent beauty.” This trend highlights a mature, sophisticated market where affluent consumers are confidently investing in enduring assets like fine jewelry and high-end watches, while local players are successfully capturing this domestic momentum; American-native luxury brands posted robust results, growing by roughly 10% to 15% year-on-year in the first quarter.

India: The New Frontier

India is the fastest-growing luxury market in the world, projected to reach $15 billion in 2026. The rise of the Indian billionaire class and the HENRYs (High Earners, Not Rich Yet) is creating massive demand for luxury cars, jewelry, and high-end wedding couture. Global houses are now prioritizing Mumbai and Delhi with the same intensity they once reserved for Shanghai. Ferrari recently hosted its first-ever national test drive event at the Buddh International Circuit, marking a transformative moment for the Indian luxury automotive landscape.

Europe and Japan: Tourism-Driven

Europe remains the largest market, accounting for approximately 30% of global luxury goods sales in 2025. However, the region has faced challenges in early 2026. International tourism spending plummeted by nearly 20% in February, primarily due to the absence of visitors from the Middle East amid the regional conflict. This demographic saw a contraction of between 15% and 25% in its consumer base. These factors severely impact the luxury sector in the region, which is structurally dependent on affluent travelers.

Japan solidified its position as the standout performer of 2025, fueled by yen weakness that made Japan a “global luxury hub” attracting massive tourist flows, particularly from China and Southeast Asia, where prices were often 20–30% lower than in home markets.

The Great Divergence: Luxury Services Outpace Goods

Perhaps the most investable structural trend within luxury today is the widening performance gap between luxury goods and luxury services. While sales of personal luxury goods have been contracting in recent years (2023-2025), luxury travel and hospitality have been growing, creating a two-speed luxury economy that offers a distinct investment outlook.

The Data: A Tale of Two Sectors

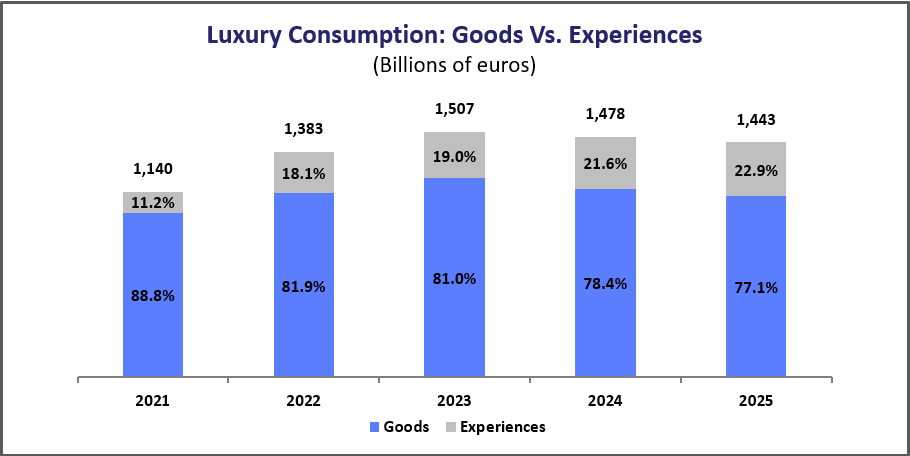

The divergence is stark. In 2025, luxury goods sales fell 2–5% while global luxury hospitality spending is projected to reach $390 billion by 2028, up from $239 billion in 2023. Experiential luxury spending has grown from 11.2% of total luxury consumption in 2021 to 22.9% in 2025 — more than doubling its share in four years.

STR data shows luxury hotels posted RevPAR (revenue per available room) growth of 5.3% through mid-2025, while economy hotels declined 1.8%. In 2026, CoStar forecasts luxury hotels to produce the strongest RevPAR metrics of any segment. Resonance Consultancy’s 2026 report found top 1% US households spend $12,400 per trip — up 48% from 2022. A Flywire survey found 79% of luxury travellers plan to spend more in 2026, with 24% expecting to spend much more, and only 1% expecting to spend less.

Why the Shift Is Structural, Not Cyclical

According to Euromonitor, over 70% of affluent consumers now place more value on experiences than material goods. Some designer clothes and bags are now ubiquitous among the well-off middle class — eroding the exclusivity that justified premium pricing. Experiential luxury cannot be mass-produced and is inherently scarce. Social media has accelerated this: a once-in-a-lifetime trip to Bhutan or an Antarctic expedition generates the same social currency as a Birkin bag, but carries the added cachet of being unrepeatable.

LVMH launched its Belmond sleeper train in Britain and is building a 230-metre, 54-suite Orient Express yacht with Accor, which offers highly exclusive, immersive, and heritage-driven experiences. Bulgari and Armani have opened branded hotels. Dolce & Gabbana and Burberry have paired with hotel groups for pop-up stores and beach clubs. The Accor Group aims to expand the share of cash flow from its luxury segment from 35% to 50% by 2030.

Investment Implications: A New Lens for Luxury Indices

For index construction and portfolio design, the goods-versus-services divergence creates a meaningful opportunity. A luxury index that overweights experiential and hospitality exposure — companies like Hyatt, The Ritz-Carlton Yacht Collection’s parent Marriott, and high-end mobility names like Ferrari and Bombardier — while maintaining selective exposure to goods companies with pricing power (Hermès, Brunello Cucinelli) could capture the structural shift while hedging against the cyclical weakness in mass-market luxury goods.

The risk is that luxury hospitality firms repeat the mistakes of luxury goods firms: over-expanding supply and diluting exclusivity. CoStar forecasts global luxury hotel rooms will climb from 1.8 million to nearly 2.2 million by 2030. Pricing discipline and controlled scarcity — the principles that have made Hermès resilient — will be the differentiator in luxury services. The emergence of ultra-luxury cruise operators and “new-scale” hospitality with sub-150-key properties paired with branded residences all point to a segment that is evolving to maintain exclusivity even as it scales.

Companies to Watch July 2026 (Billions of USD)

| Company | Sub-Industry | Mkt Cap | YTD Δ |

|---|---|---|---|

| Hermès International SCA | Personal Luxury & Apparel | 188.00 | -23.4% |

| Compagnie Financière Richemont SA | Personal Luxury & Apparel | 131.00 | 6.2% |

| Christian Dior SE | Personal Luxury & Apparel | 92.85 | -23.5% |

| Ferrari NV | High-End Mobility & Transportation | 65.76 | 0.7% |

| Bombardier Inc | High-End Mobility & Transportation | 23.56 | 46.6% |

| Hyatt Hotels Corporation | Luxury Hospitality, Gaming & Financials | 17.65 | 16.9% |

| Chow Tai Fook Jewellery Group Ltd | Personal Luxury & Apparel | 14.58 | -8.7% |

| Brunello Cucinelli | Personal Luxury & Apparel | 6.11 | -19.2% |

| Ermenegildo Zegna NV | Personal Luxury & Apparel | 3.58 | 30.3% |

| Bains Mer Monaco | Luxury Hospitality, Gaming & Financials | 3.55 | 28.8% |

| EIH Limited | Luxury Hospitality, Gaming & Financials | 2.10 | -11.0% |

| Salvatore Ferragamo SpA | Personal Luxury & Apparel | 1.88 | 21.8% |

| Sanlorenzo SpA | High-End Mobility & Transportation | 1.50 | 25.7% |

| Ferretti SpA | High-End Mobility & Transportation | 1.12 | -4.8% |

Source: MarketScreener.com, Yahoo Finance

2030 Outlook: Structural Growth Despite Cyclical Pain

By 2030, abstracting from the current critical geopolitical headwinds, the global luxury market is projected to reach a valuation of between €2.0 and €2.5 trillion, implying a compound annual growth rate of 5–9%. Unlike the reactionary spending seen in the early 2020s, this growth phase is underpinned by a broadening consumer base and a fundamental shift in buyer behavior — luxury as lifestyle, asset class, and experience. China is projected to increase its share of luxury consumption, becoming one of the top markets alongside the US and Europe. India is also emerging as a major growth engine for the sector, driven primarily by explosive domestic wealth generation; the luxury market is projected to expand up to 3.5 times by 2030, compared to 2025.

The industry is also entering an era of hyper-efficiency thanks to the widespread integration of generative AI, which Deloitte’s latest report identifies as one of the most transformative forces shaping the sector’s future. AI is expected to increase profits by optimizing supply chains and reducing unsold inventory. By 2030, the most successful luxury conglomerates will be those that have evolved into comprehensive luxury lifestyle ecosystems, where the primary asset is not the product itself, but the relationship between brand and customer maintained through data-driven personalization.

Conclusion: A Sector Worth Watching Closely

The luxury sector in mid-2026 presents an unusual combination: long-term structural tailwinds colliding with both acute geopolitical stress and cyclical headwinds. These include a shrinking aspirational customer pool, the redefinition of Chinese luxury consumption, and the consequences of years of counterproductive aggressive strategies. On the other hand, the global HNWI population continues to grow. The winners will be companies focused on upper and ultra-luxury products, with authentic brand equity and strategic management of artificial scarcity, and those positioned in the faster-growing experiential luxury segment.

For investors with a medium-to-long-term horizon, the present dislocation may represent an attractive entry point. But the thesis is now selective rather than sector-wide. In a world of heightened uncertainty, the case for luxury remains compelling — provided one distinguishes between the brands that have earned their pricing power and those that merely borrowed it during the boom.

References

- Capgemini: World Wealth Report 2026 – https://www.capgemini.com/insights/research-library/world-wealth-report/

- Bain & Company: Luxury in Transition — Securing Future Growth – https://www.bain.com/insights/luxury-in-transition-securing-future-growth/

- Bain & Company: 2025 Chinese Personal Luxury Goods Market – https://www.bain.com/insights/the-2025-chinese-personal-luxury-goods-market/

- McKinsey: Global Luxury Hospitality Outlook – https://www.mckinsey.com/industries/travel/our-insights/the-state-of-tourism-and-hospitality-2024

- Morgan Stanley: LVMH Sector Review – https://www.investing.com/news/analyst-ratings/morgan-stanley-cuts-lvmh-stock-price-target-on-weaker-growth-outlook-93CH-4560610

- J.P. Morgan: Luxury Market Outlook – https://www.jpmorgan.com/insights/global-research/retail/luxury-market

- BNP Paribas: 2026 Luxury Goods Sector Outlook – https://cib.bnpparibas/2026-luxury-goods-sector-outlook/

- Deloitte: Global Powers of Luxury 2026 – https://www.deloitte.com/global/en/industries/consumer/perspectives/global-powers-of-luxury.html

- Euromonitor: Beyond Possessions — The New Landscape of Luxury – https://www.euromonitor.com/article/beyond-possessions-the-new-landscape-of-luxury

- Resonance Consultancy: 2026 Future of Luxury Travel – https://resonanceco.com/reports/future-of-luxury-travel/

- STR / CoStar: 2026 US Hotel Industry Outlook – https://www.costar.com/products/str-benchmark/resources/data-insights-blog/us-hotel-forecast-assumptions-february-2026

- PwC: Emerging Trends in Real Estate — Hospitality Outlook – https://www.pwc.com/us/en/industries/financial-services/asset-wealth-management/real-estate/emerging-trends-in-real-estate-pwc-uli/property-type-outlook/hospitality.html

- The Economist: Luxury goods are out, but luxury travel is in – https://www.economist.com/business/2025/10/06/luxury-goods-are-out-but-luxury-travel-is-in

- Deutsche Bank: Perspectives 2026 Annual Outlook – https://wealth.db.com/en/insights/investing-insights/economic-and-market-outlook/cio-annual-outlook-2026-investing-in-tomorrow.html

- United Nations: Population Division – https://population.un.org/dataportal/data/indicators/70/locations/900/start/1999/end/2030/table/pivotbylocation?df=b087a3da-086d-4ebf-bfc5-b037cd994034

- CNBC: Iran war wipes out $100 billion from luxury stocks – https://www.cnbc.com/2026/03/27/iran-war-wipes-out-100-billion-from-luxury-stocks.html

- Yahoo Finance: Europe Luxury Firms Lose $176 Billion As War Hits Demand – https://finance.yahoo.com/markets/stocks/articles/europe-luxury-firms-lose-176-170124767.html

- Yahoo Finance: Ferrari Stock Is Down 33% Since July 2025: 1 Reason the Market Is Wrong – https://finance.yahoo.com/markets/stocks/articles/ferrari-stock-down-33-since-095100709.html

- LVMH: LVMH continues to achieve organic growth in the first quarter, in a global environment impacted by the conflict in the Middle East – https://www.lvmh.com/en/publications/lvmh-continues-to-achieve-organic-growth-in-the-first-quarter-in-a-global-environment-impacted-by-the-conflict-in-the-middle-east

- CNBC: Luxury stocks spike on proposed U.S.-Iran peace deal; LVMH up 5% – https://www.cnbc.com/2026/06/12/luxury-stocks-lvmh-hermes-burberry-iran-war-peace-deal.html

- Morgan Stanley: Luxury Outlook: From Contraction to Caution – https://www.morganstanley.com/insights/articles/luxury-goods-market-outlook-2026-contraction-to-caution

- Bain & Company: Finding a New Longevity for Luxury – https://www.bain.com/insights/finding-a-new-longevity-for-luxury/

- Capgemini: World Wealth Report 2003 – http://www.theiafm.org/publications/38.pdf

- Sothebys: Higher Hermès Bag Prices in 2026: What You Need to Know – https://www.sothebys.com/en/articles/higher-hermes-bag-prices-in-2026-what-you-need-to-know

- Luxury Pulse: Ferrari F80 Sales – https://luxurypulse.com/sales/show/6168-ferrari-f80-for-sale

- Vogue College: Quiet Luxury and Timeless Desire: How Hermès Mastered Luxury – https://www.voguecollege.com/articles/london/quiet-luxury-and-timeless-desire-how-hermes-mastered-luxury/

- BSPK: Luxury Retail Trends 2025: Navigating U.S. Tariffs and Global Trade Tensions – https://www.bspk.com/post/luxury-retail-trends-2025-navigating-u-s-tariffs-and-global-trade-tensions

- Reuters: Ferrari, Maserati halt Middle East deliveries due to war – https://www.reuters.com/world/middle-east/ferrari-suspends-middle-east-deliveries-due-war-2026-03-19/

- Reuters: Gucci sales extend falls as Iran war clouds de Meo's Kering turnaround – https://www.reuters.com/business/gucci-sales-extend-falls-iran-war-clouds-de-meo-turnaround-2026-04-14/

- Bain & Company: Finding a New Longevity for Luxury – https://www.bain.com/insights/finding-a-new-longevity-for-luxury/

- India Forbes: Why luxury's biggest bet on India might be its costliest mistake – https://www.forbesindia.com/article/thought-leadership/essec-business-school/why-luxurys-biggest-bet-on-india-might-be-its-costliest-mistake/2993422/1

- Bain & Company: Global luxury stabilizes amid compounding disruptions as brands race to amplify meaning and rebuild relevance – https://www.bain.com/about/media-center/press-releases/2026/global-luxury-stabilizes-amid-compounding-disruptions-as-brands-race-to-amplify-meaning-and-rebuild-relevance/

- McKinsey: The State of Fashion 2025 – https://www.mckinsey.com/~/media/mckinsey/industries/retail/our%20insights/state%20of%20fashion/2025/the-state-of-fashion-2025-v2.pdf